Content accounting: Calculating value of content in the enterprise

The challenge of content value

Content value is a hot topic in marketing and technical communication. In the publishing industry, the connection between content and value is clear. A publisher sells a book (or film or other piece of content) and gets book sales, ticket revenue, or streaming subscriptions in return. But what if your content is a part of the product (like user documentation) or used to sell the product (like a marketing white paper)? In these cases, measuring content value is much more challenging.

It is tempting to fall back on measuring cost instead of value. The cost of content development can be a trap, though. Eliminating wasted effort and optimizing content workflows is sensible, but too much focus on cost leads us toward content as a commodity.

Content should not be treated as a commodity. Good content:

Persuades people to choose a specific product

Enables people to understand complex technical concepts

Reduces product returns

Helps people use products correctly and thereby avoid injuries or costly errors

Eliminates the need for a call to technical support

Burnishes a company’s reputation

Good content delivers business value.

This white paper proposes a framework for measuring content value based on accounting principles.

Accounting principles

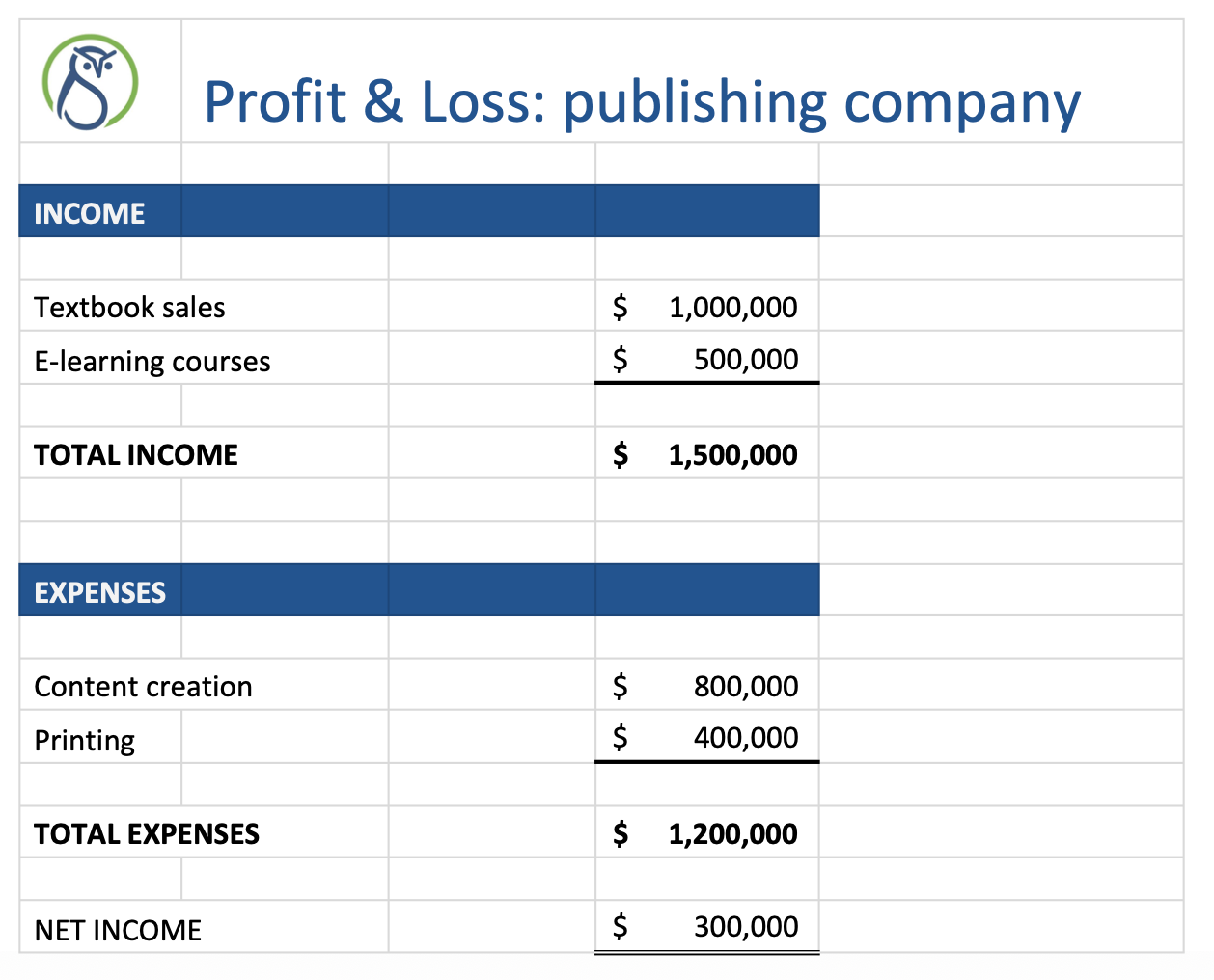

Financial accounting starts with two basic documents: a profit and loss statement (P&L) and a balance sheet.

The P&L shows income and expenses over time. For content accounting purposes, the expense side is straightforward—it lists salaries, rent payments, and other costs. The income side shows payments from customers for products and services. A content-focused company can align income (for example, book sales or a website subscription) with the expenses (such as salaries for writers, website infrastructure, editing expenses, and printing expenses).

Figure 1. Simplified P&L for a publishing company

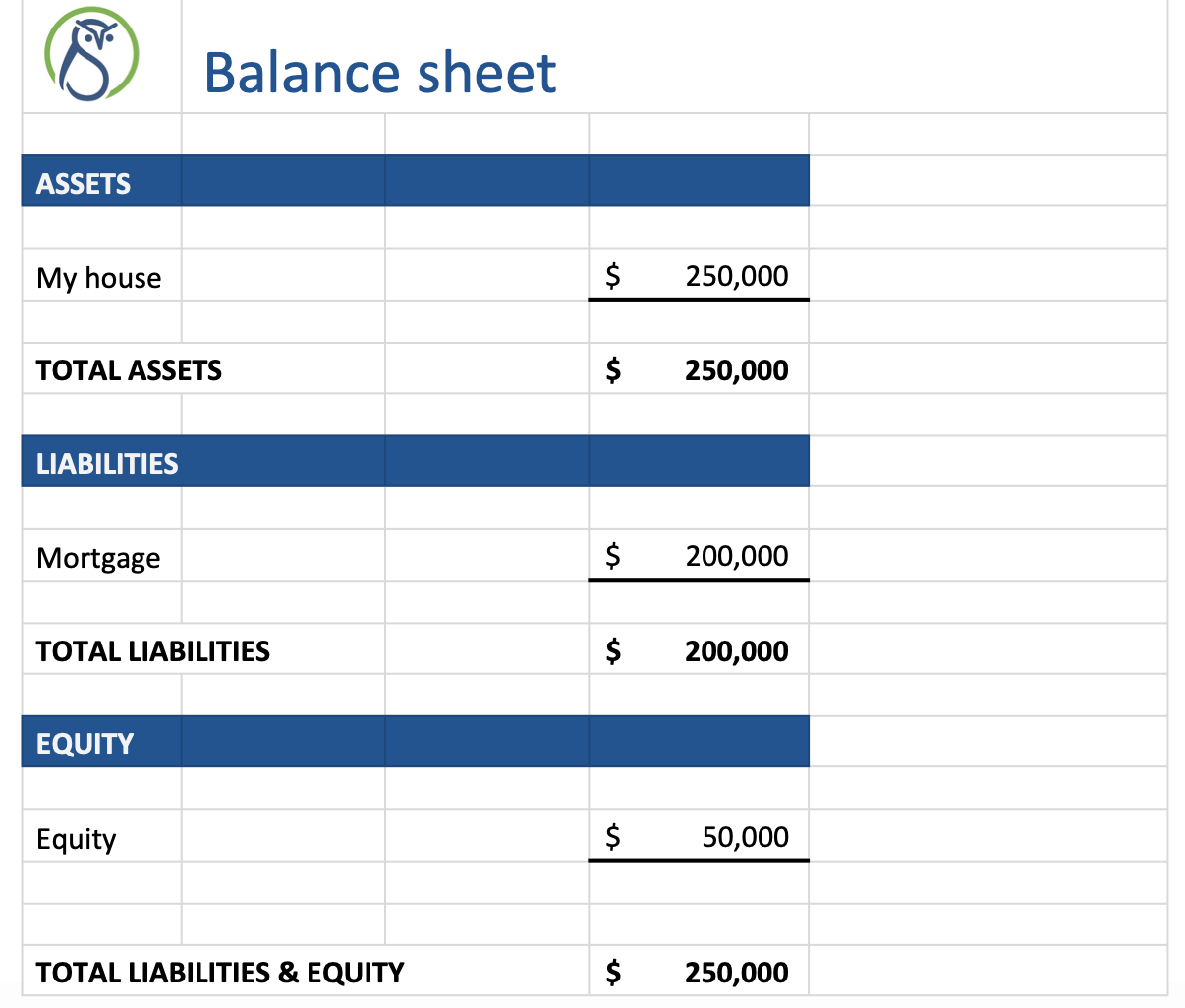

The balance sheet lists assets, liabilities, and equity. Assets minus liabilities always equals equity. The best-understood example of this is a house. If you own a house worth $250,000 and have a $200,000 mortgage, then your equity is $50,000.

Figure 2. Simplified balance sheet for a homeowner

In a business context, assets are items that have long-term value, such as office buildings and equipment. For a coffee shop, a high-end espresso machine might be listed as an asset. Many organizations also include the value of intellectual property, especially if they hold a patent. Liabilities include bills that need to be paid and long-term debt. Organizations may also list expected liabilities, such as anticipated product returns or legal liabilities due to product defects.

In an organization where content plays a supporting role, content expenses are usually measured, but not content-related income, assets, or liabilities.

Creating a content P&L

To create a content-focused P&L, you need to measure income and expenses related to content.

Income

To measure income, we have chosen to focus on contributions based on a hierarchy of business needs.

Compliance

If your company is regulated, compliance is a key reason that you have content. Unless you deliver the content required by regulators, you cannot sell the product. Some industries where compliance is important include:

Pharmaceuticals and life sciences: Drug labels and material safety data sheets must follow formats specified by the U.S. FDA and other regulatory agencies. Medical device documentation is also regulated.

Heavy machinery: Operating instructions for industrial equipment sold in the European Union are regulated by the EU’s machinery directive.

Insurance and finance: Insurance policies must meet different requirements in each state in the U.S. Financial documents may require specific formats and contents.

Producing documents that meet compliance requirements is a cost of doing business. Without compliant content, the organization cannot participate in the market. On the content P&L, we recommend setting compliance-related income as a percentage of the overall product income. In determining the amount, measure the cost of content development as a percentage of product development.

Cost avoidance

In content workflows, we can reduce costs in several ways:

Efficiency: To improve efficiency, we look for ways to squeeze out waste from the content development process. One common area for improvement is review workflows—reducing the number of people who review content, ensuring that reviews are focused, and providing for concurrent instead of serial reviews.

Reuse: For technical content especially, reuse is a powerful way to reduce costs. Reuse means less total content to maintain, which in turn reduces the overall cost of ownership and downstream localization costs.

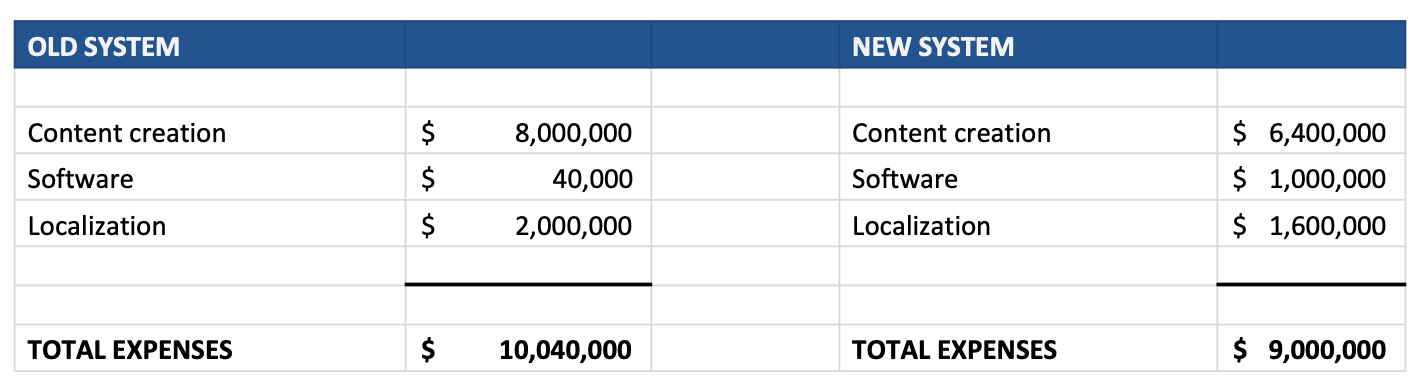

Automation: Formatting automation is another powerful way to reduce the overall cost of content development. An upfront investment in publishing software can result in eliminating 30–50% of recurring content development efforts.1

Efficiency, reuse, and automation are typically used to justify an investment in publishing software or improved workflows. Cost avoidance doesn’t create additional income, but it does mean increased productivity.

Figure 4. Cost avoidance via software investment

In addition to a systems argument, consider a few additional possibilities for cost avoidance:

Product liability: Especially in the United States, legal liability is a concern. Injuries resulting from use or misuse of a product can be reduced or avoided by providing better content. This in return reduces the company’s legal exposure (and uninjured customers tend to be happier customers). Reuse helps ensure that all content is current and accurate, thus reducing potential liability.

Product returns: One rough estimate is that $17B are lost annually due to product returns of consumer electronics.2 Up to 20% of these returns are because customers cannot understand how to use a product, as opposed to an actually defective product. Improve product content to reduce the rate of product returns.

Technical support costs: Technical support calls are one-to-one, and staffing call centers is complex. By contrast, an article that answers a common question is written once and then consumed by many customers. Investing in useful, searchable technical support content is usually less expensive than providing live technical support.

Revenue growth

Content can drive revenue growth. To support revenue growth, consider the following:

Content marketing: Invest in useful persuasive content to spread the word about your organization’s product. Improve the reach of your content with search engine optimization.

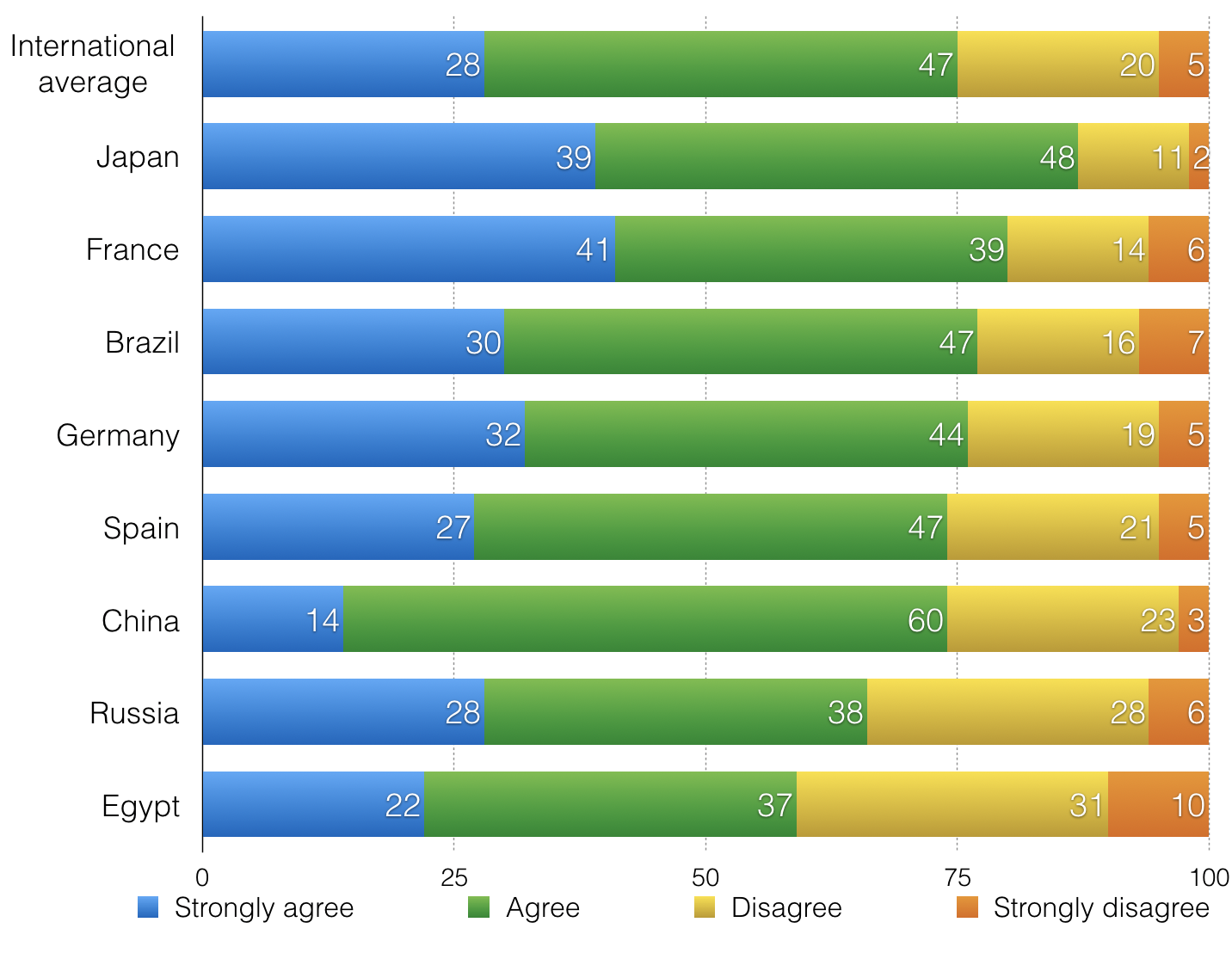

Localization: To broaden global reach, invest in local languages. In a Common Sense Advisory research survey, 75% of respondents agreed or strongly agreed that “When faced with the choice of buying two similar products, I am more likely to purchase the one that has product information in my language.”3 Figure 5. Survey question: “When faced with the choice of buying two similar products, I am more likely to purchase the one that has product information in my language.” (source: Common Sense Advisory)

Improve product content: Better product content means fewer product returns (discussed in cost avoidance), better reviews, and happier customers. All of these factors contribute to repeat business and market share growth.

Competitive advantage

Beyond good search, SEO, and localization, content can provide a direct competitive advantage. For an example, consider King Arthur Flour, which sells a variety of flours. King Arthur Flour does well on a basic Google search for “flour,” but they are in a sea of other possibilities. But someone at the company went deeper. Many people in their target audience are baking from scratch. To improve baking results, flour should be measured by weight rather than volume. So as a baker, a common search would be “how much does flour weigh.” And here, you see that King Arthur Flour owns the results.

Figure 6. King Arthur Flour gets the coveted featured snippet and the first result for “how much does flour weigh”

The link takes the reader to a handy chart that lists weights for several different flour varieties. So King Arthur has now captured the attention of potential customers.

Figure 7. The ingredient weight chart

Branding

Your content can contribute the overall company brand identity. Marketing, technical, and product content can all support the company’s brand. A prestige brand needs to have content that supports premium position. A product with friendly, informal positioning (such as the Slack messaging platform) needs content that matches.

Figure 8. The help content uses Slack branding, both in appearance and in tone

Expenses

Most organizations have a good understanding of the content creation expenses. These include:

Employee salaries and related costs

Facilities

Software

Travel

Education

If you do not have access to these costs within your organization, a reasonable estimate is $100/hour for content creators in North America. (That amount assumes a staff employee and includes benefits and all additional expenses.)

Based on a loaded hourly cost, you can work out the total cost of staff. For contractors and vendors, use the amounts on their invoices.

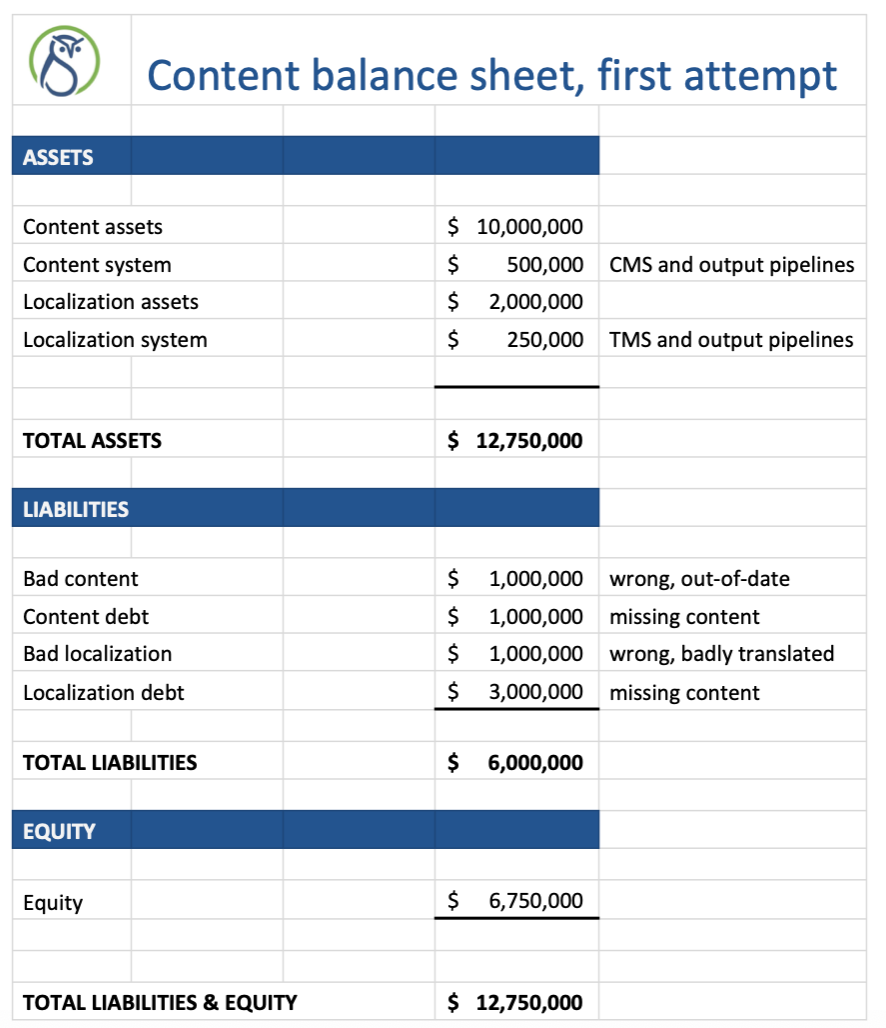

Creating a content balance sheet

A balance sheet lists assets and liabilities. In general accounting, an asset is something that has long-term value, either cash or something that can be converted into cash, like real estate. A liability is a debt, such as a bank loan or an outstanding credit card balance.

Assets

For your balance sheet, you need to measure the value of content assets that have long-term value to the business, including:

Content, such as white papers, product content, and other in-depth information

Content management systems and output pipelines

Content development assets, such as glossaries, terminology standards, and style guidelines

Content taxonomies

Content models

Localization assets, especially translation memory and multilingual terminology

Localization management systems and output pipelines

We also need to think about depreciation—the idea that an asset can lose its value over time. A car, for example, starts out with a certain value. After 10 years, the car is worth a lot less than it was when it was first purchased. Most content assets also depreciate—after a few years, a white paper is out of date. So the content balance sheet needs to be updated periodically to capture the change in value for the various assets.

Here are some factors that affect content value:

Accuracy

Relevance

Targeted to the right audience

Useful to the targeted audience

Accomplishes its purpose (for example, describes a product’s features and benefits or explains a concept)

Longevity

Localization-friendly

Certain factors serve as content value multipliers:

Reuse: Is the content used in multiple locations?

Content variants: Does the content enable you to create multiple versions from a single source?

Multichannel output: Can the content be delivered to multiple output formats automatically?

Is there a localized version of this content in your repository?

Liabilities

Liabilities reduce the value of your content. Your liabilities are content debt—the work that needs to be done to bring your content up to the needed standard (or to create it).4 They include the following:

Bad content experience: The information is unattractive, hard to understand, and/or inaccessible.

Out of date: The information needs to be updated.

Wrong audience: The information is targeted at the wrong audience. For example, a document intended for patients in a hospital uses complex medical terminology that only medical professionals would understand.

Wrong voice and tone: The information does not meet the organization’s standards for voice and tone. For example, a casual game company would likely use informal language, so a formal, legalistic document would be the wrong voice and tone.

Offensive: The information uses offensive language or stereotypes.

Wrong format: The information does not use the format preferred by the consumer of the information.

Badly translated: The information is available in the target languages, but the translation is poor, so it leaves the reader with a bad impression.

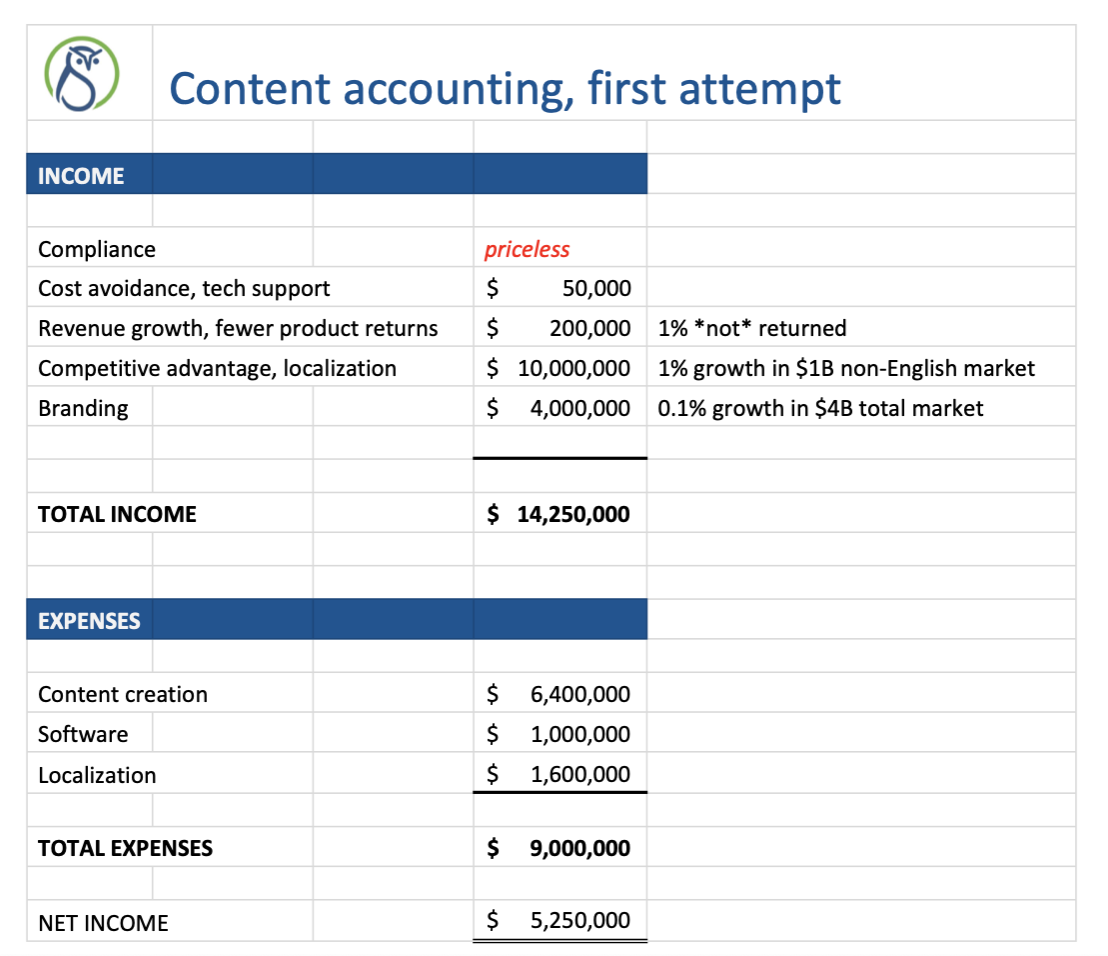

Putting it all together

So at this point, you can put together your first content accounting reports.

Industry estimates are that writers working in Microsoft Word spend 30–50% of their total time on formatting. Moving to systems that separate content and formatting eliminates that formatting time.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

Al M.

Solid material here. Kinda sad that the “how do we value content” discussion may now fade away.